ON THIS PAGE…

Form DRC-01B

In December 2022, the Government of India introduced Rule 88C to the Central Goods and Services Tax (CGST) Rules, 2017. Rule 88C allows automated notifications to be sent to taxpayers if there is any mismatch between their GSTR-1/IFF and GSTR-3B. Notifications will be sent when the tax liability furnished in the GSTR-1/IFF exceeds the tax paid in the GSTR-3B by a defined threshold amount and percentage.

The taxpayer has to pay the differential tax liability, along with interest under Section 50, by using Form GST DRC-03, or taxpayers have to explain the differences in the tax payable within seven days. Regardless of the action, taxpayers must reply to the notification using Part B of Form GST DRC-01B.

Filing Form DRC-01B Part B

To file Form DRC-01B Part B:

- Go to the GST portal.

- Click Login on the top right corner of the page.

- On the following page, enter your GST Username and Password and click Login.

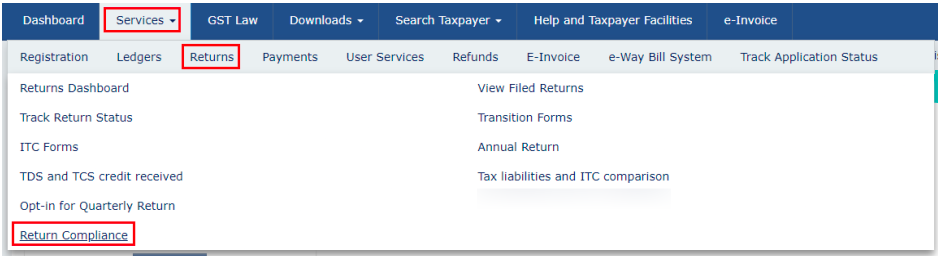

- Click Services at the top.

- In the dropdown, hover over Returns and select Return Compliance.

(or)

- Click Return Compliance in the Dashboard.

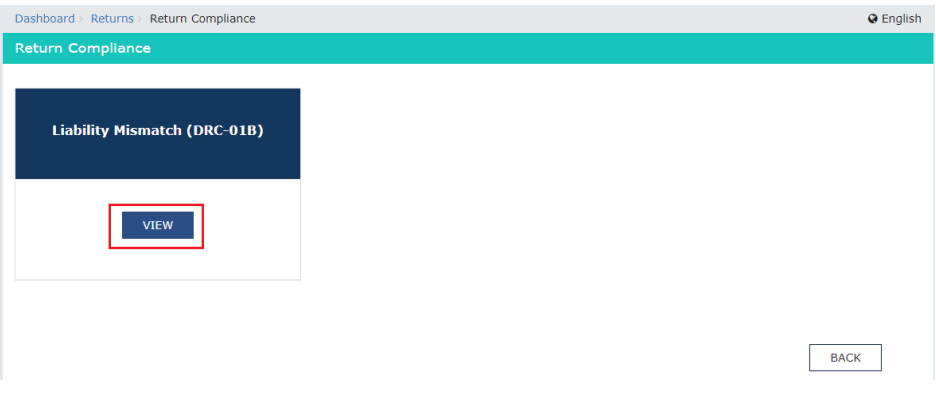

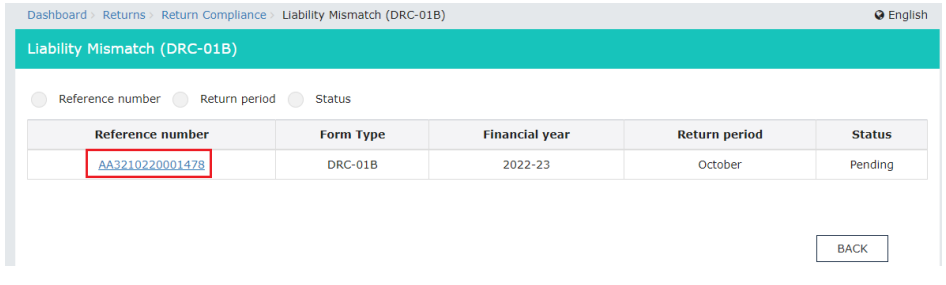

- On the Return Compliance page, click View in the Liability Mismatch (DRC-01B) tile.

- On the Liability Mismatch (DRC-01C) page, you can view the acknowledgement number of all the return periods for which you received the notification in Form DRC-01B Part A.

Insight: You can also select from the Reference number, Return period, or Status options at the top and search for the acknowledgement number.

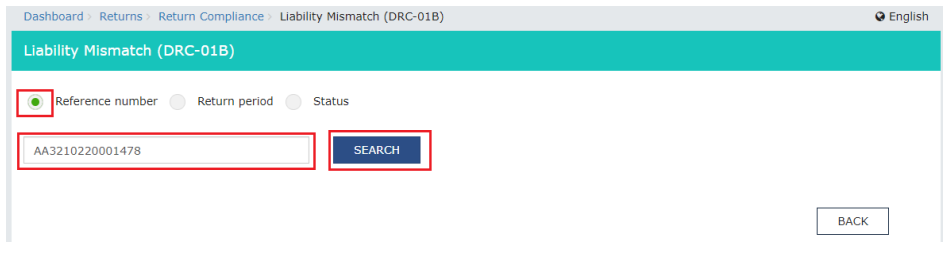

Reference Number

If you select Reference number, enter the ARN and click Search.

If the status of the record is Pending, you can file Form DRC-01B.

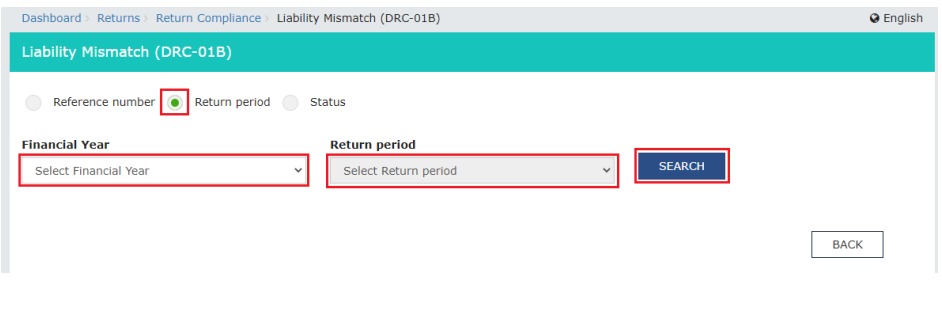

Return Period

If you select Return period:

- Select the financial year for which you want to file Form DRC-01B from the dropdown below the Financial Year field.

- Select the return for which you want to file Form DRC-01B from the dropdown below the Return period field.

- Click Search.

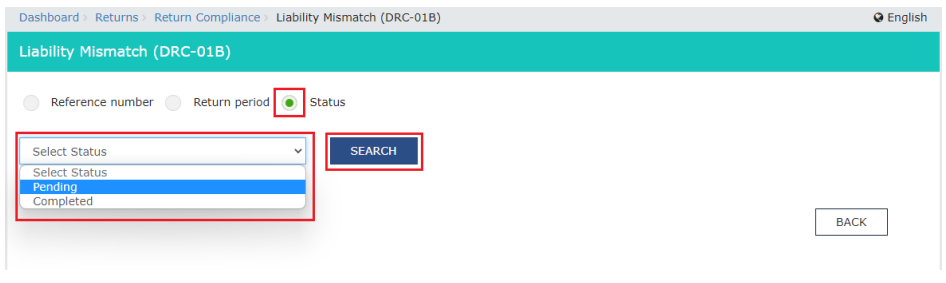

Status

If you select Status, select either Pending or Completed as the status and click Search.

- Click the Reference number for the period for which you want to file Form DRC-01B.

The Form DRC-01B for the ARN entered will be displayed. It contains two parts: Part A and Part B.

Part A contains the Intimation of Difference in Liability Reported in Statement of Outward Supplies and that Reported in Return details.

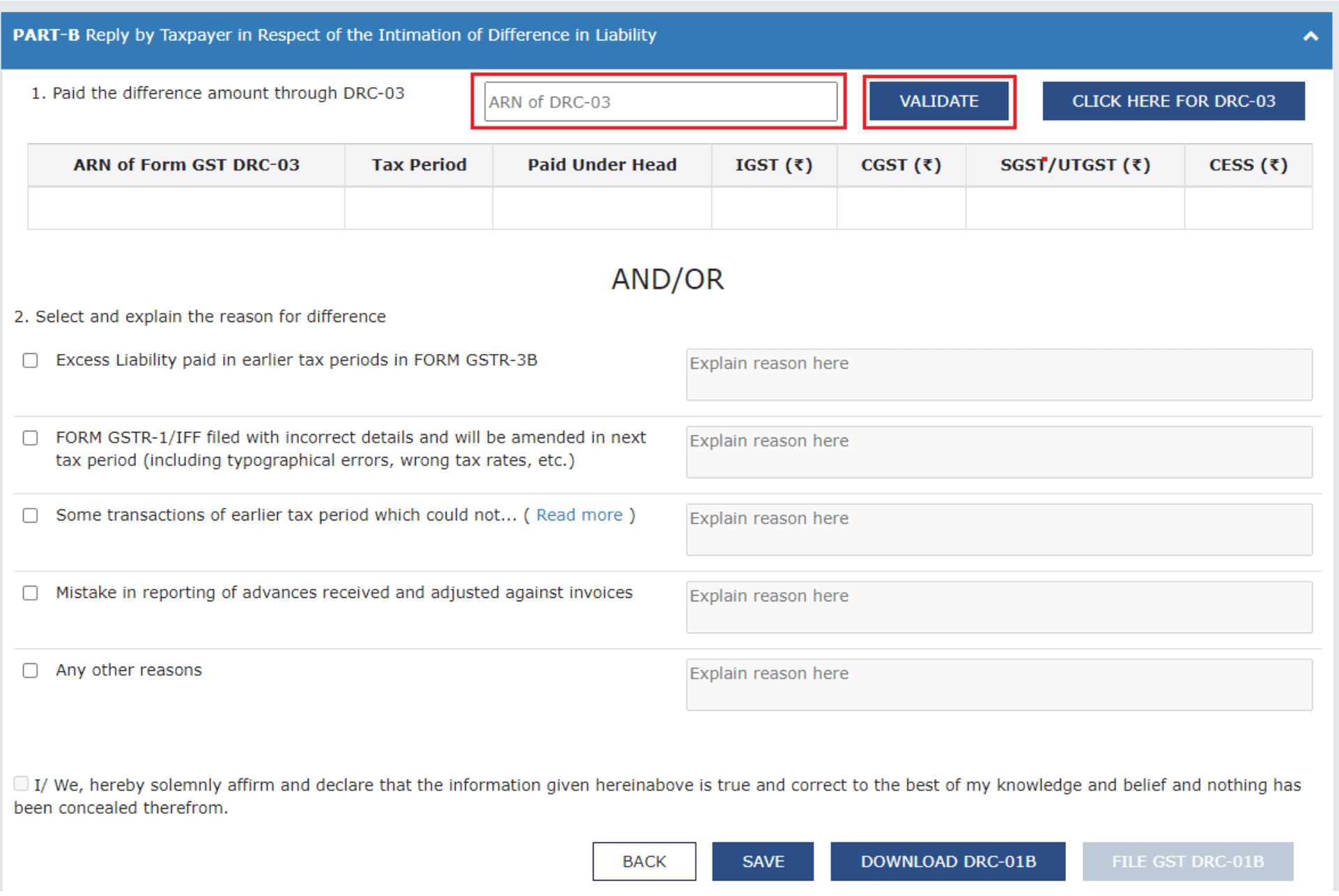

Part B contains the Reply by Taxpayer in Respect of the Intimation of Difference in Liability details. it is further divided into two sub-parts. In subpart 1, you can make payment for the Difference in Liability Repor****ted. In subpart 2, you can select a Reason for the Difference in Liability Reported and provide further explanation for the same.

As a taxpayer, you’ll have to make a payment for the Difference in Liability Reported or select a Reason for the Difference in Liability Reported and provide further explanation for the same in Part B.

Make Payment for the Difference in Liability Reported

To make payment for the difference in liability reported:

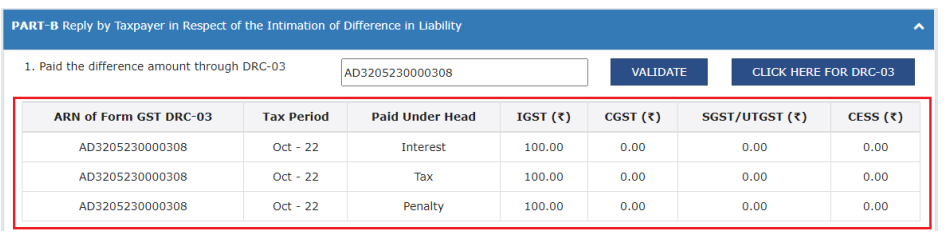

- In the 1. Paid the difference amount through DRC-03 section of the Part B of Form DRC-01B section, enter the acknowledgement number of the period for which you received the DRC-01B Part A notification in the ARC for DRC-03 text box.

- Click Validate.

The summary of the payment details that have been paid through DRC-03 towards the difference in liability reported will be displayed.

-

If you get the error message “Please provide valid ARN for DRC-03”, check the following:

- Ensure that the ARN is valid and that it corresponds to the DRC-03 and GSTIN for which you received the DRC-01B Part A notification.

- Verify that the cause of payment specified in DRC-03 is Liability mismatch - GSTR-1 to GSTR-3B.

- The DRC-03 has been filed on or after the date on which you received the DRC-01B Part A notification was issued.

- The overall tax period aligns with the period for which of the DRC-01B Part A notification was issued.

- If you file your GSTR-3B return every month, ensure that the from and to dates match the period.

- If you file your GSTR-3B return every quarter, ensure that the period covers at least one month within the quarter.

-

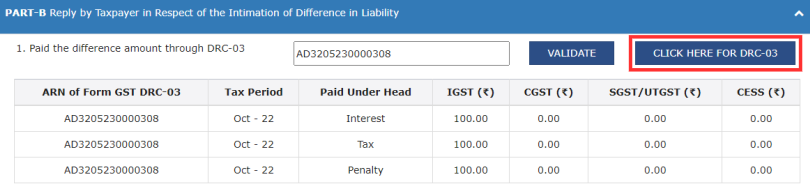

If you haven’t made payment for the difference in liability reported, click Click Here for DRC-03.

Select the Reason for the Difference in Liability Reported

To select a reason for the difference in liability reported:

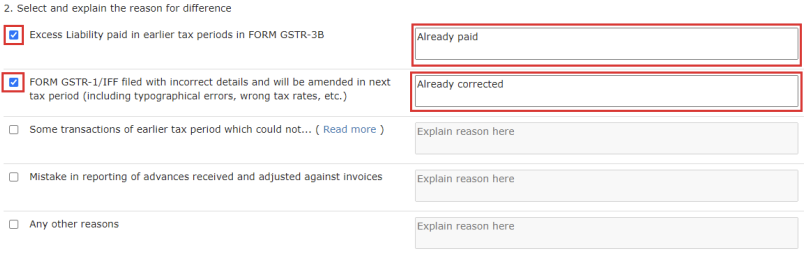

- In the 2. Select and explain the reason for difference section of the Part B of Form DRC-01B section, check the checkbox with the relevant reason and provide a detailed explanation in the text box next to the reason. The reason can be up to 500 characters.

- If the reason is not specified, check the Any other reason option and provide a detailed explanation in the text box next to it.

- Click Save.

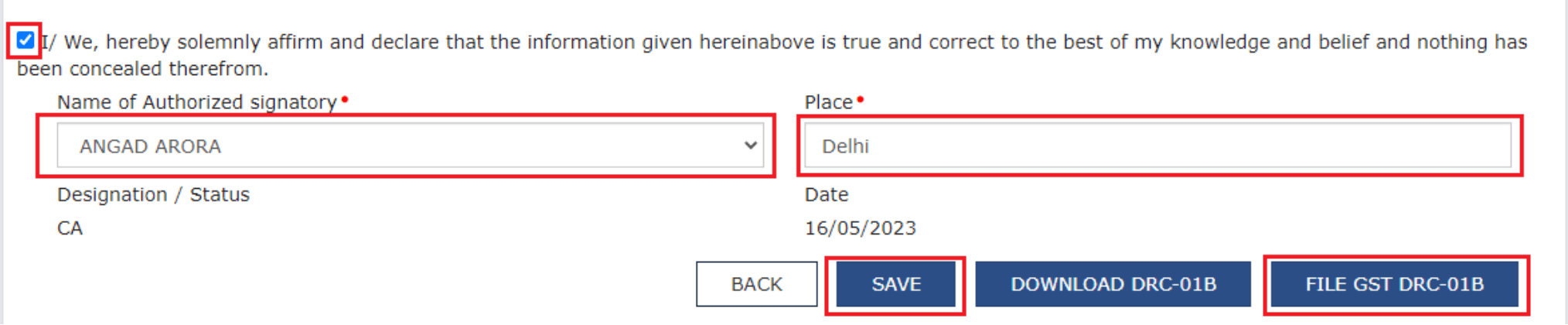

- Check the declaration check box at the bottom. The checkbox will be enabled only after you click Save.

- Select the Name of the authorized signatory from the dropdown below the field and enter the Place in the text box below the field. The Designation/Status and Date fields will be auto-populated.

- Click Save. You’ll get a notification that the details have been saved.

- Click File GST DRC-01B. This button will be enabled only when you check the declaration checkbox and enter the required details in it.

- Click Download DRC-01B. A system-generated draft order will be downloaded into your system as displayed. Check the draft order carefully to rule out any discrepancies.

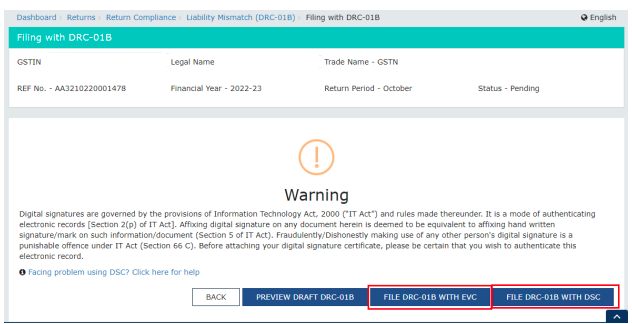

- In the pop-up that appears, click Proceed.

- On the following page, you can choose whether you want to file using an Electronic Verification Code(EVC) or a Digital Signature Certificate(DSC). Click File DRC-01B With EVC or File DRC-1B With DSC.

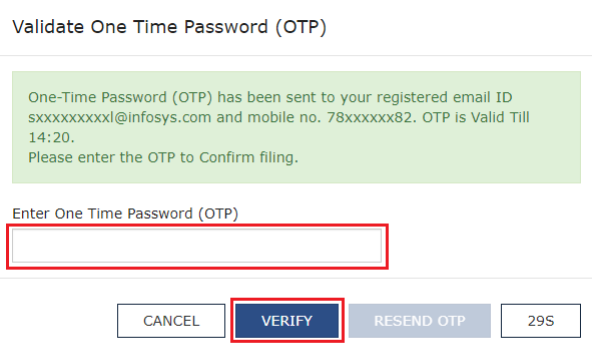

- Enter the OTP sent to the email address and mobile number of the primary authorized signatory registered on the GST portal, and click Verify.

Note: If you don’t receive the OTP within 30 seconds, you can click Resend OTP to get a new OTP. You can request a new OTP up to 3 times.

- In the pop-up that appears, click OK.

You have filed your reply to the DRC-01B Part A notification. You can check the status from the Status option.

To know more about Form DRC-01B, read our FAQs on Form DRC-01B.

Warning: If you don’t respond in Form GST DRC-01B within 7 days from the date on which you received the notification, then your GSTR-1/IFF will be blocked for the subsequent tax periods. This will continue until you either deposit the amounts specified in the notification or provide an explanation for non-payment.

Yes

No

Yes

No

Thank you for your feedback!

Thank you for your feedback!