Section 206AB and Section 206CCA are not separate new sections but are special provisions that have been introduced in the Income Tax Act, 1961 through the Finance Act, 2021.

Section 206AB (TDS) allows you to deduct tax at source (TDS) at a higher rate for non-filers of Income Tax returns.

Section 206CCA (TCS) is a similar provision to collect tax at source at a higher rate from non-filers of Income Tax returns. This section is effective from 1 July 2021.

The sections, 206AB and 206CCA, are effective from 1 July 2021.

You will have to deduct TDS as per Section 206AB if the vendor meets all the following conditions:

For example, if the current FY is 2021-2022, then we must check if the time limit to file the income tax return for FY 2020-2021 has expired. If yes, you must consider FY 2019-2020 and FY 2020-2021. If it has not expired, then you must consider FY 2018-2019 and FY 2019-2020, provided the aggregate total amount of TCS & TDS in those years in more than ₹50,000.

To make this easier for businesses, the Ministry of Finance has released a Compliance Check Functionality which will help you identify if the vendor meets the conditions mentioned above. Read More

The tax must be deducted at the following rates, whichever is the highest:

Scenario: Kumar has a bill and in general, he must deduct TDS of 5% under Section 194H. His vendor did not file the IT returns and he matches the criteria that we have mentioned above. In this case, according to the new provision, Kumar must deduct TDS under Section 194H at a rate of 10%, at twice the rate specified in the relevant provision of the Act.

This provision is not applicable for:

If PAN is not furnished by your vendor, then under Section 206AA, you would already be deducting TDS at a higher rate. If both the Section 206AA and Section 206AB is applicable to your vendor, then the TDS shall be deducted at the highest of the two rates.

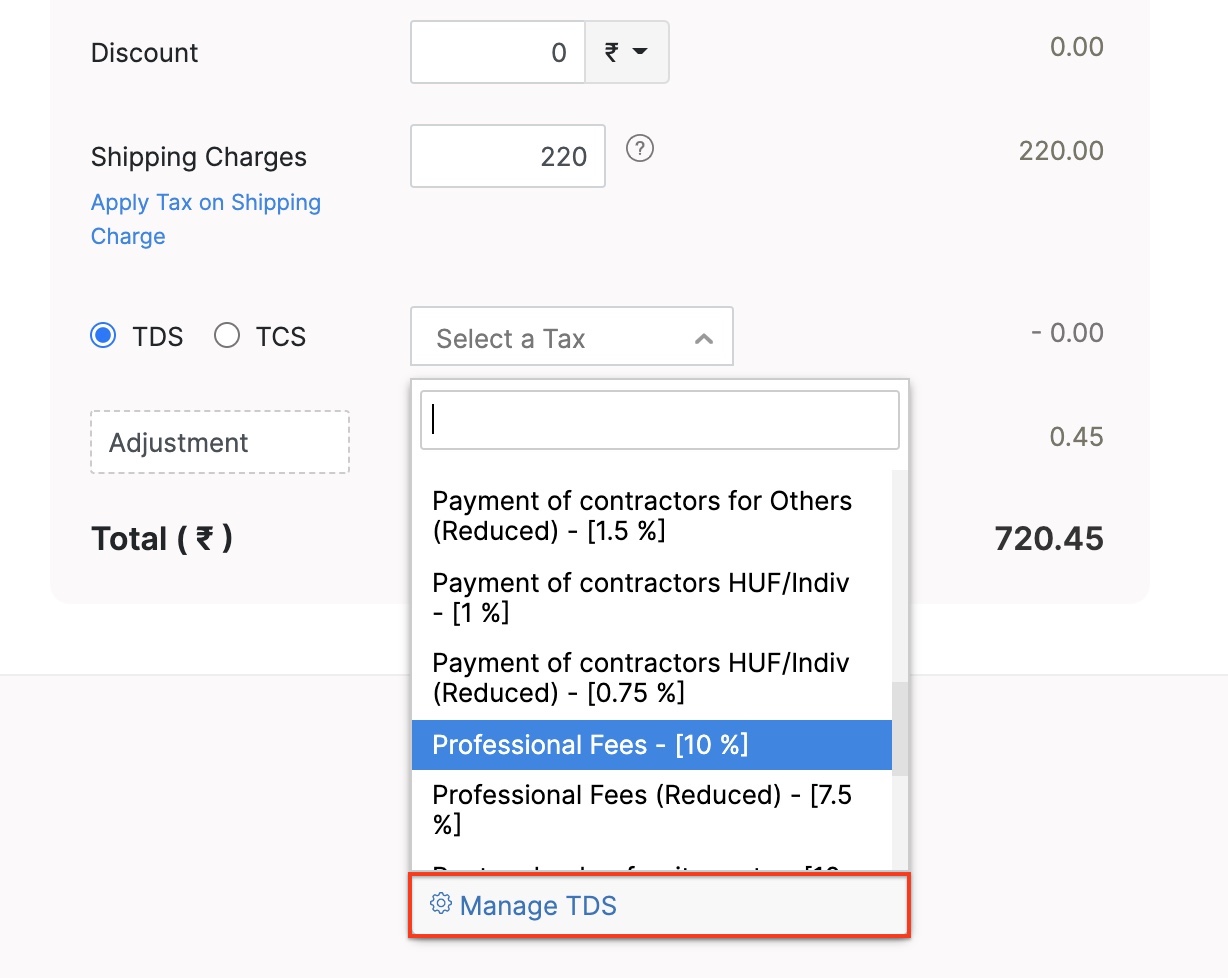

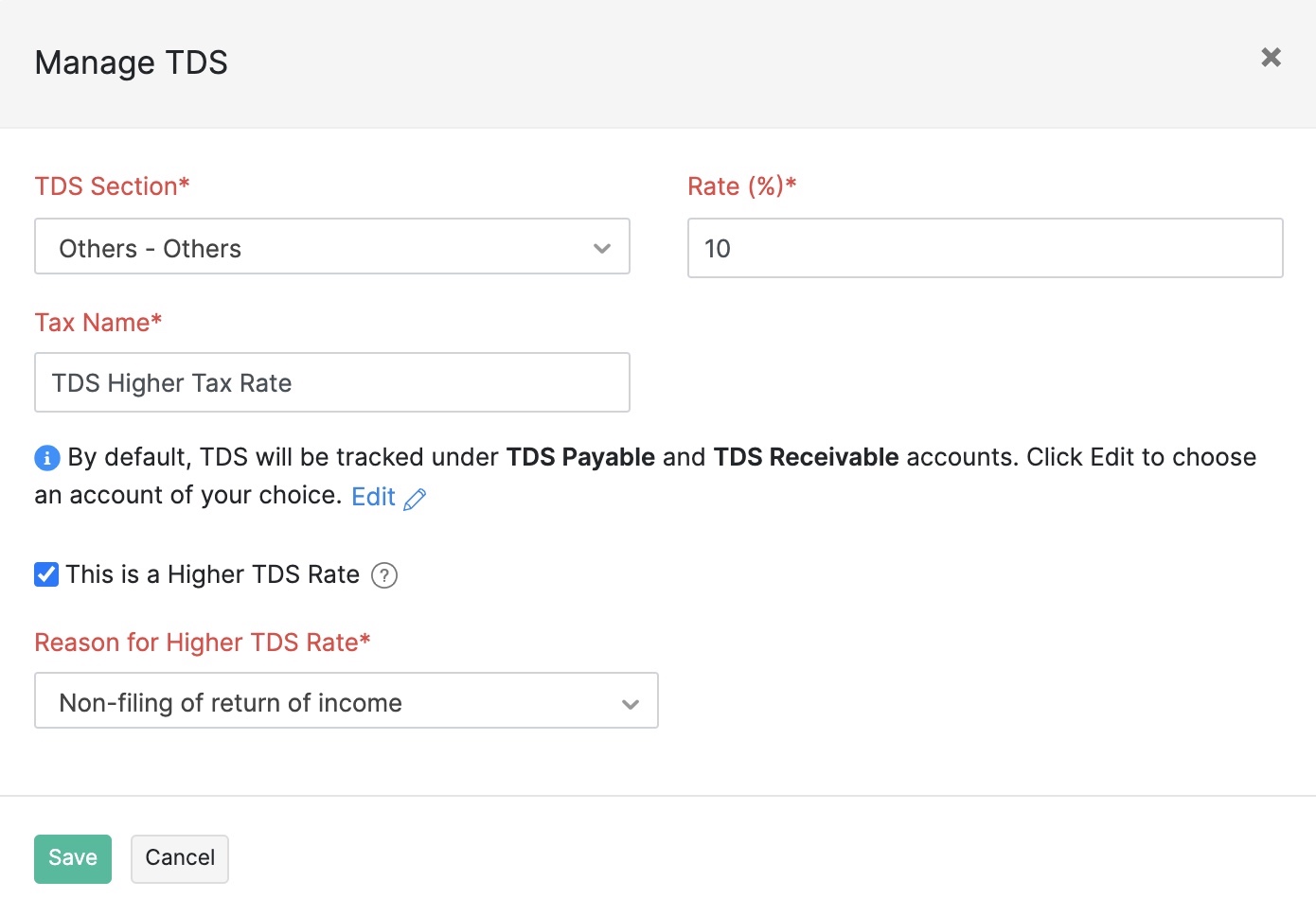

To create a TDS tax with a higher rate:

Now, a TDS tax with a higher rate will be created and applied to the purchase transaction.

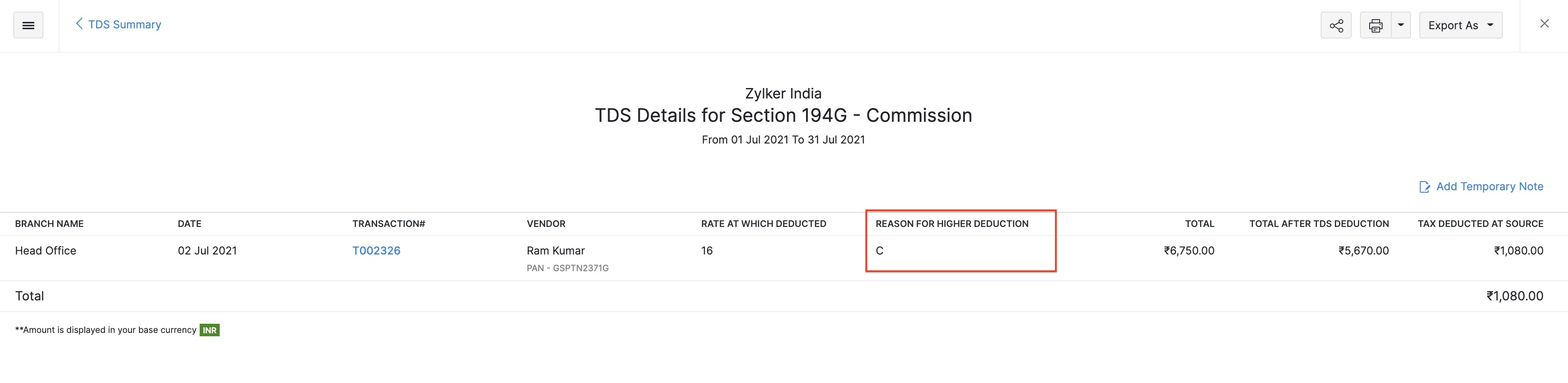

You can track the higher TDS rate using the TDS Summary report. You will find a new column, Reason for Higher Deduction, which will contain the following values which correspond to the reason for which they were applied to the transaction.

| Value | Reason |

|---|---|

| C | Non-furnishing of PAN |

| U | Non-Filing of Income Tax return |

The value in this column will be U, if the TDS is deducted at a higher rate under Section 206AB.

You must collect tax at source from customers or buyers if:

For example, if the current FY is 2021-2022, then we must check if the time limit to file the income tax return for FY 2020-2021 has expired. If yes, you must consider FY 2019-2020 and FY 2020-2021. If it has not expired, then you must consider FY 2018-2019 and FY 2019-2020, provided the aggregate total amount of TCS & TDS in those years in more than ₹50,000.

To make this easier for businesses, the Ministry of Finance has released a Compliance Check Functionality which will help you identify if the customer meets the conditions mentioned above. Read More

TCS must be collected at the following rates, whichever is the highest:

Scenario: Priya has an invoice and in general, she must collect TCS under Section 206C 1H (0.1%). Her customer did not file the IT returns and the customer matches the criteria mentioned above. So, according to the new provision, Priya will have to collect TCS under Section 206C 1H with a rate of 5% (at the rate of five percent).

It is not applicable for a non-resident Indian who does not have a permanent establishment in India.

If PAN is not furnished by your customer, then under Section 206CC, you would already be collecting TCS at a higher rate. If both Section 206CC and 206CCA is applicable to your customer, then the TCS shall be collected at the higher of the two rates.

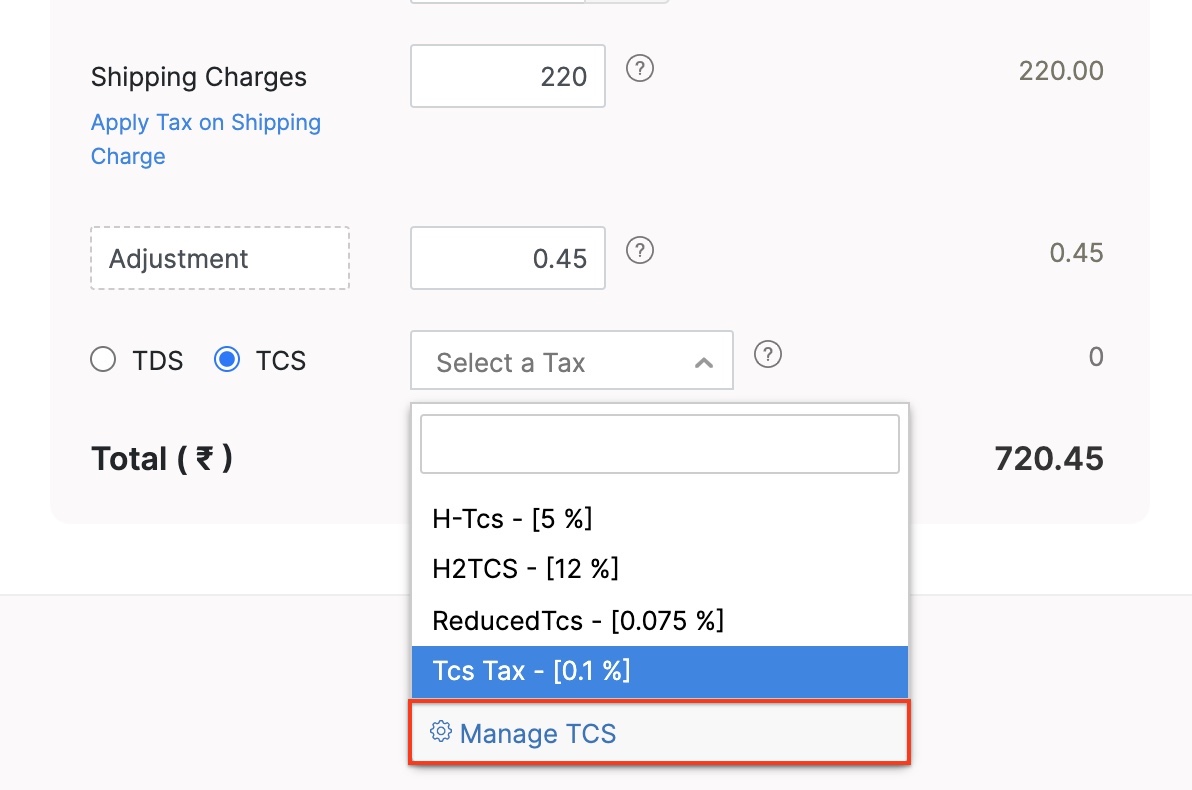

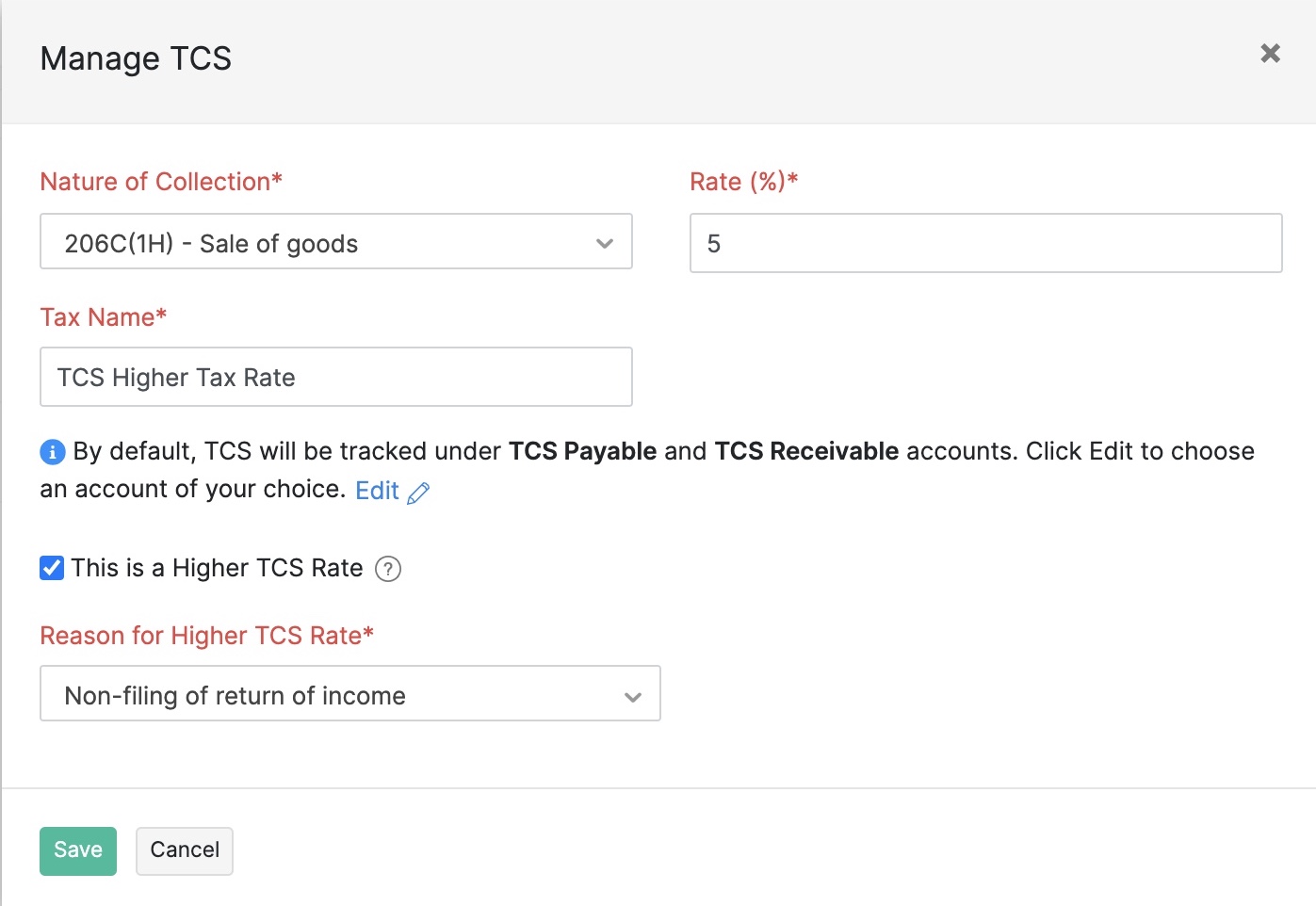

To create a TCS tax with a higher rate:

Now, a TCS tax with a higher rate will be created and applied to the transaction.

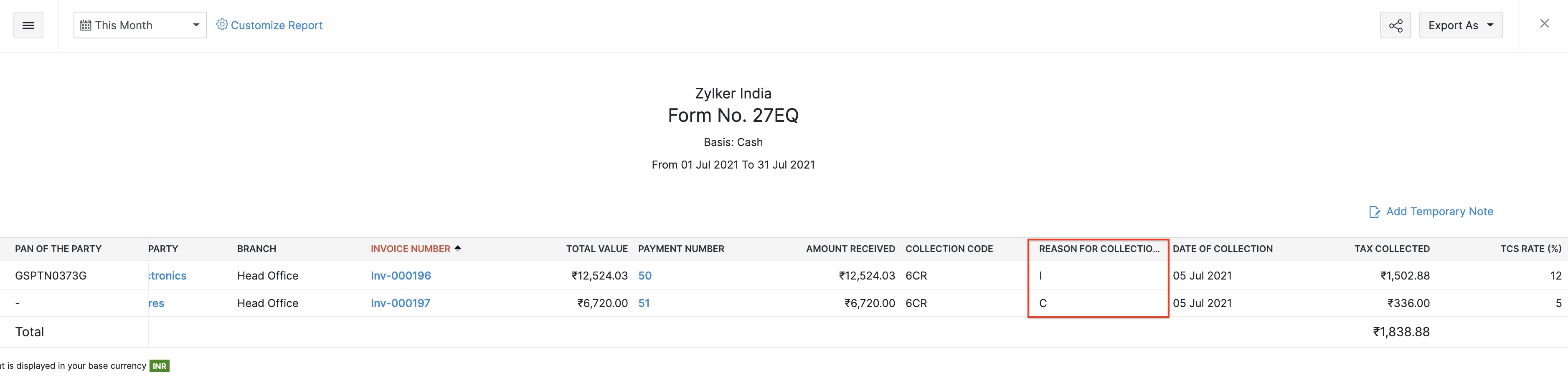

You can track the higher TCS rate using the Form 27EQ report. You will find a new column, Reason for Collection at Higher Rate, which will contain the following values which correspond to the reason for which they were applied to the transaction.

| Value | Reason |

|---|---|

| C | Non-furnishing of PAN |

| I | Non-Filing of Income Tax return |

The value in this column will be I, if the TCS is deducted at a higher rate under Section 206CCA.

To facilitate this option, the Ministry of Finance has released a Compliance Check Functionality for Section 206AB & Section 206CCA.

Here’s how tax deductors or collectors can use the Compliance Check Functionality:

In Zoho Books, if Section 206AB is applicable for the PAN, you can create a new higher TDS rate and set the same as the default TDS rate for the vendor having the PAN. By doing this, whenever you create a bill for this vendor, the associated TDS rate will be applied to the transactions.

Yes

No

Yes

No

Thank you for your feedback!

Thank you for your feedback!

Available in all mobile platforms

Books

Simplify accounting

and GST filing.